An Update of STATS SA data & Other Selected Leading Economic Indicators: December 2010

Â

Â

Â

Â

Â

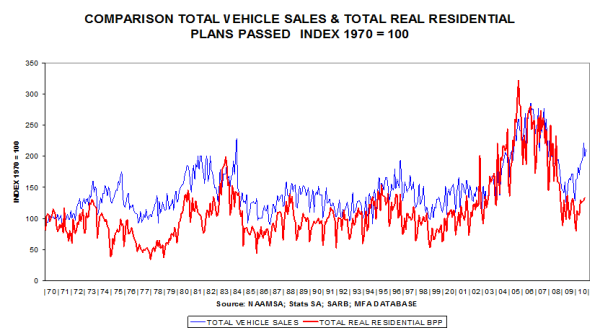

This comparison reflects “big ticket items” – vehicle sales and house plans passed – both are strongly cyclical and both are sensitive to interest rate movements. Belatedly, the residential sector is improving.

The cyclical movements correspond closely; vehicle sales are almost 25% higher than a year ago and houses are 7% higher in deflated value terms.

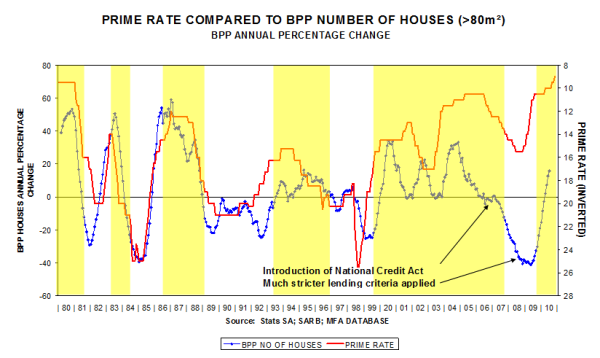

Two blows struck the private housing industry in 2007/08 but it seems to be responding belatedly to lower interest rates, currently showing a 15,8% rise over the past year (left-hand scale).

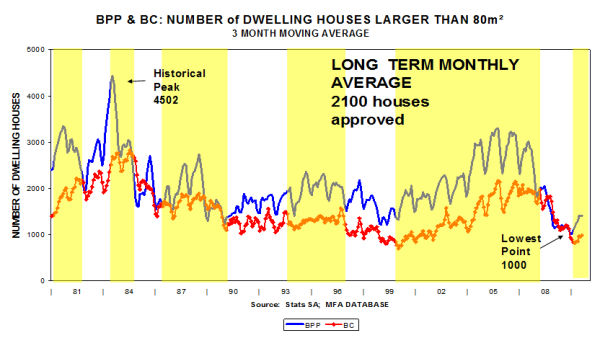

In terms of numbers, private housing is barely bouncing off the bottom.

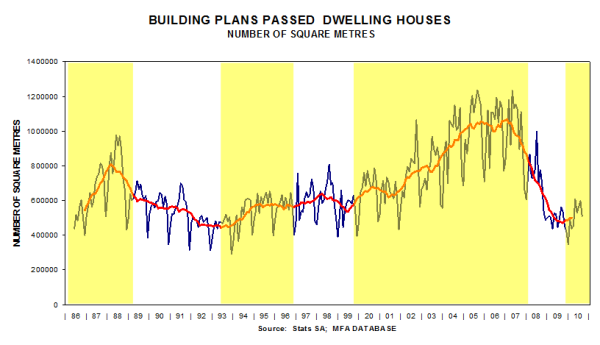

In terms of square metres, dwelling houses are bottoming out.

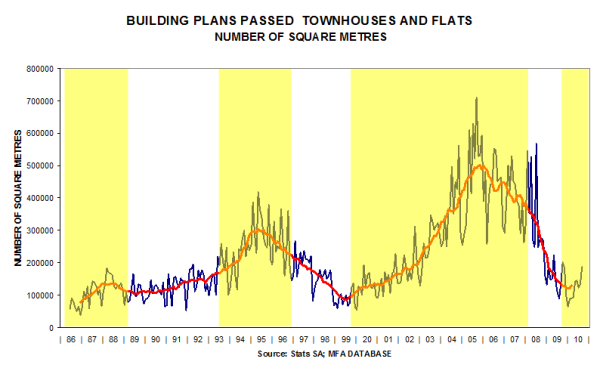

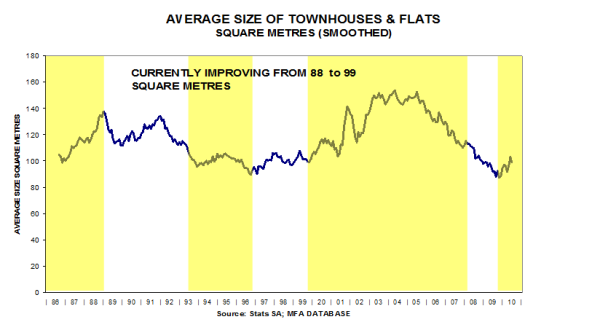

And townhouses and flats seem to be improving from very low levels.

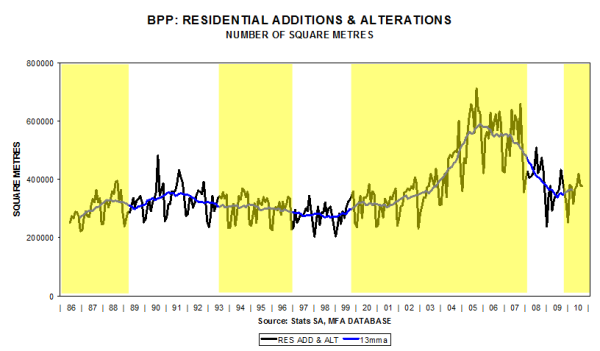

Still performing poorly but a bottoming-out is evident.

The gradual downtrend in the sizes of townhouses and flats seems to be reaching a lower turning point.

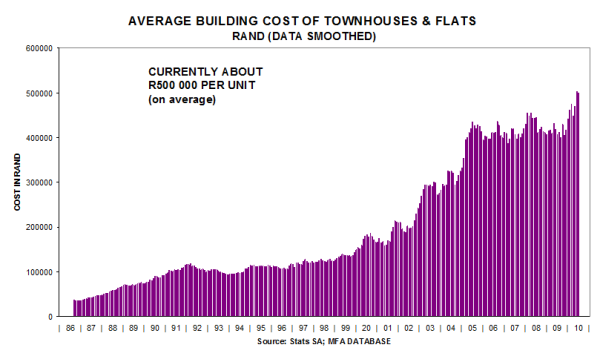

The building cost of townhouses and flats has recently risen to about R500 000 per unit.

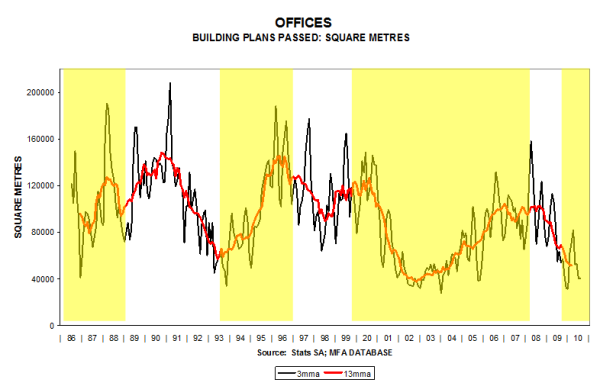

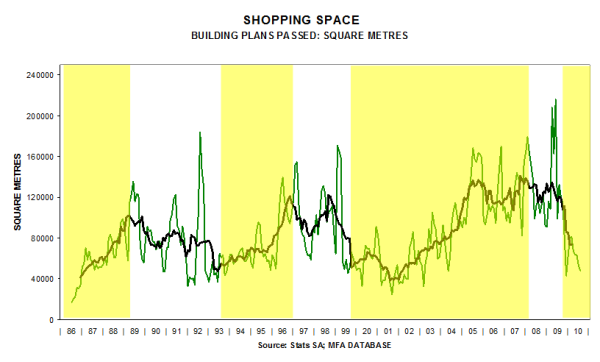

The demand for new office space has dropped to extremely low levels.

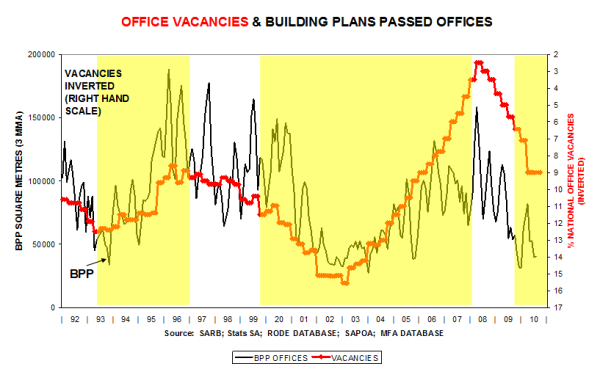

This is because office vacancies are still high on a nationwide basis (vacancies line inverted).

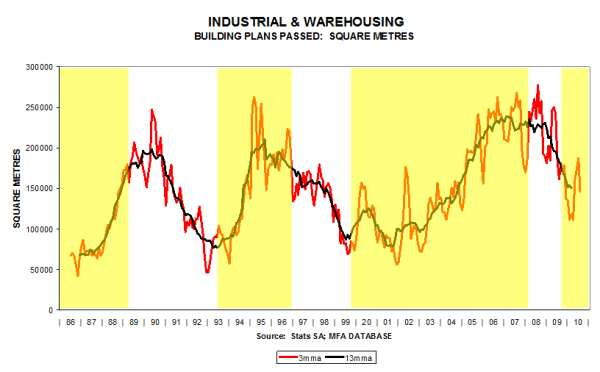

Further evidence of over-building.

It is quite likely that the trough of the cycle has been recorded.

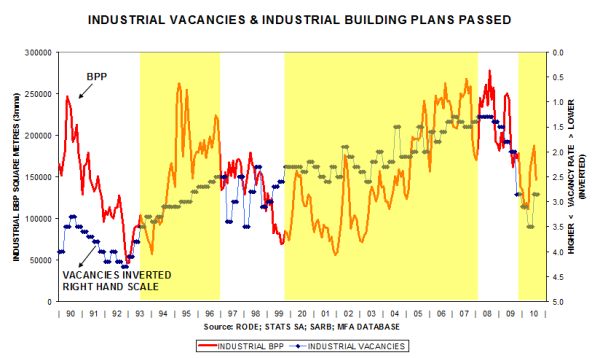

But industrial vacancies are still relatively high(vacancies line inverted).

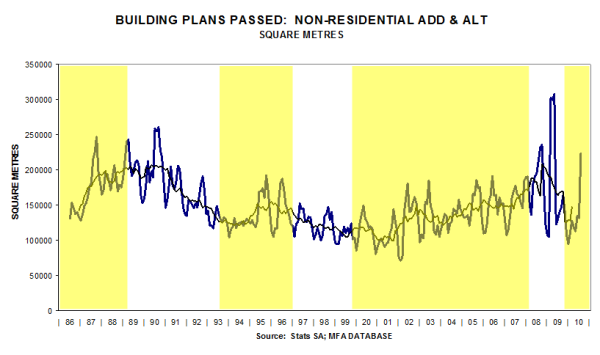

A bounce back is evident.

Some improvement from a very low level is apparent.

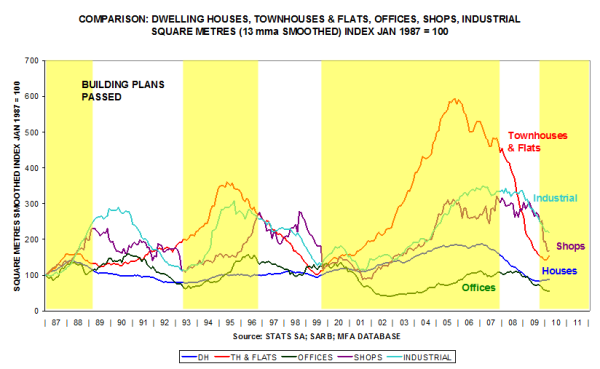

This comparison shows the relative performance of the various market segments since 1987. Houses, flats & townhouses showing signs of bottoming out.

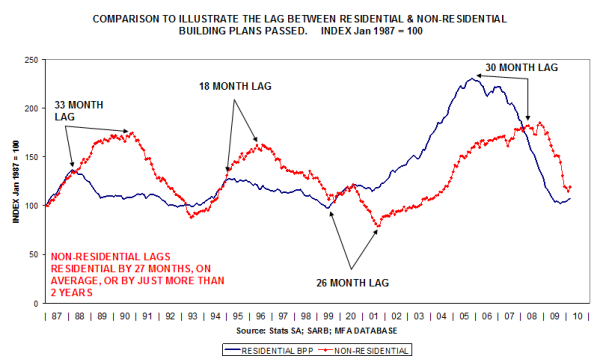

This comparison shows the lagged pattern (residential is forming a trough, non-residential has further to fall).

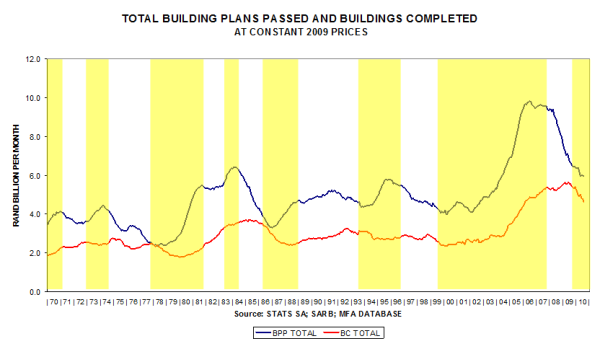

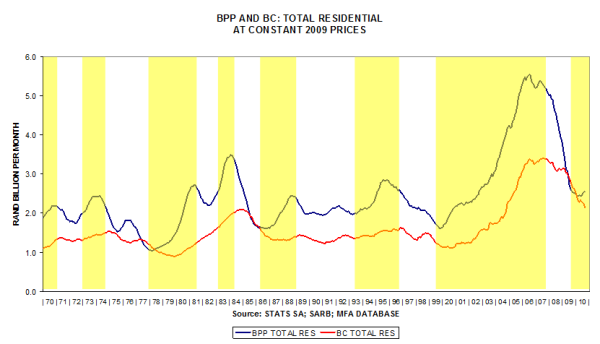

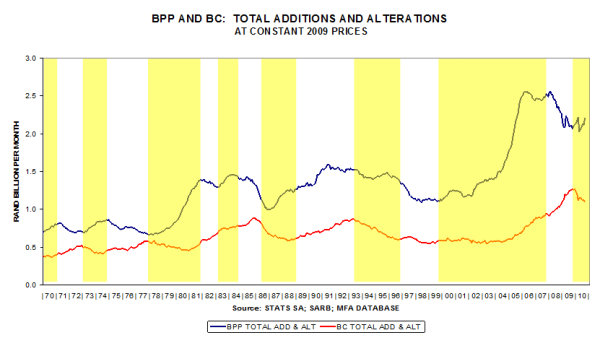

Building Plans Passed is bottoming out, and the lagging Buildings Completed time series is still tending downward.

Both indicators have further to fall.

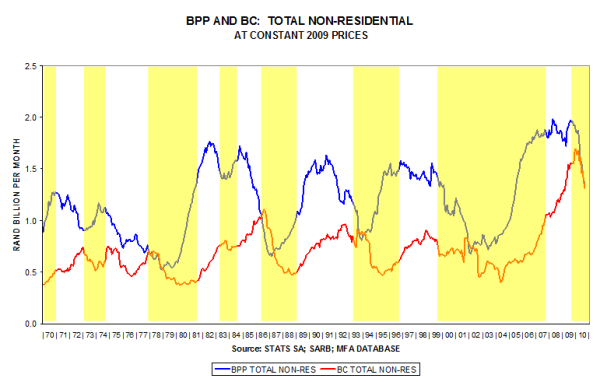

BPP could be bottoming out, BC not so.

In deflated value terms, it seems as if BPP total could be approaching a trough, but not so in the case of BC.